General Market Overview

Energy sector rally

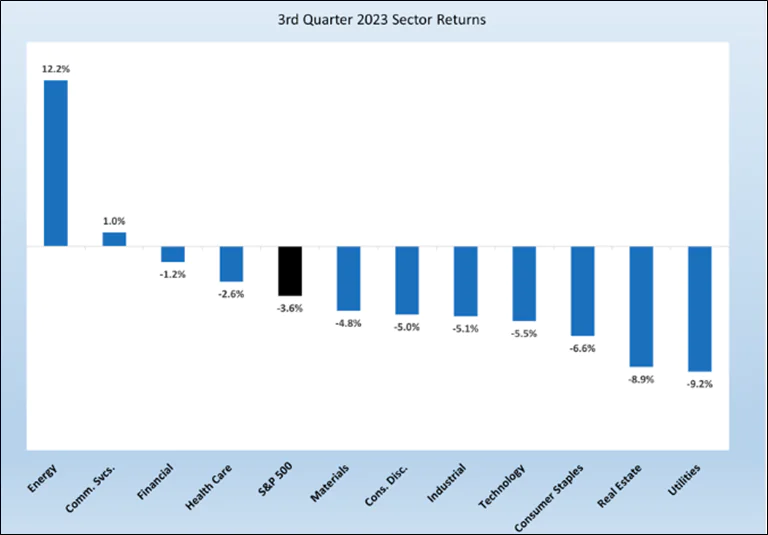

Increased geopolitical tensions and conflicts in major oil-producing regions, such as the Middle East and Russia, have led to supply disruptions. This reduced global oil output by approximately 3 million barrels per day, resulting in a significant price increase. Nonetheless, energy prices are predicted to continue rising throughout the winter later this year. The upward trajectory of oil prices has translated into increased fuel and energy costs, impacting both households and businesses, as well as contributing to inflationary pressures. Thus, as energy companies continue to restrict their historic low supply of energy, companies and their shareholders will continue to benefit. Consequently, the energy companies situated within the S&P 500, most notably oil mining companies, have rallied during Q3 despite coming at the cost of consumers benefit and are likely to continue until rates begin to fall. For example, the likes of ExxonMobil, BP and Shell gained upwards of 15% in the latest quarter.

Interest rates easement

As of the 26th of July 2023, the US Federal Reserve (FED) rose interest rates up to 5.50% to further dampen inflation, ensuring that a ‘smooth landing’ is still viable. In a similar fashion, the UK Monetary Policy Committee (MPC) rose interest rates by 0.25% to 5.25% (3rd August 2023). This came in response to concerns that inflation had not been controlled efficiently, thus, the Bank of England also deemed it necessary to raise rates. However, as we neared the end of the quarter, both the FED and the MPC undertook a review in September and concluded that their historic rate hikes have had the desired impact they were hoping for, as inflation continues to dissipate. Despite the long-term optimistic outlook for inflation and interest rates, the “higher for longer” mantra persists in relation to interest rates, highlighting the FED’s and MPC’s intention to keep interest rates where they are, until a significant change to inflation is prevalent. Consequently, this has caused US treasury yields to rise, despite interest rates remaining unchanged. This is because the demand for guaranteed yielding assets has risen, whilst riskier assets, such as equities, have fallen due to diminished consumer sentiment.

Figure 1: Q3 sector returns – November (Source: Forbes, October 2023.)

Equity struggle

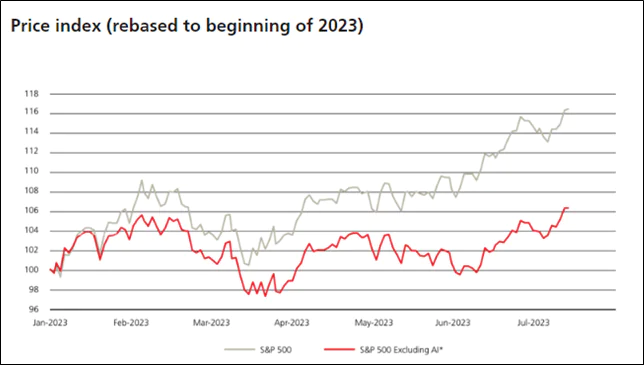

Investors entered the quarter optimistic with Federal reserve (FED) orchestrating a ‘soft landing’ for the economy. However, this optimism vanished when the FED and Bank of England (BOE) kept rates the same, installing a higher for longer mantra around interest rates. Thus, interest rate sensitive investments such as fixed interest and money market funds saw mass inflows, causing the equities market to underperform and extending diminished consumer sentiment into a slight bearish turn. The magnificent seven were able to prop up the performance of the S&P 500 during the first 2 quarters of 2023 (due to the speculation surrounding AI), but they have equally struggled in Q3. This has been reflected in the S&P500 as they account for approximately 26% of the index, whereas Energy stocks account for 5%, thus the recent energy recent rally has been overshadowed by the performance of the dismal magnificent 7. However, investors heavily anticipate that the extensive monetary policy tightening may soon come to an end, in the hope interest rates begin to fall over the coming quarters.

Figure 1: S&P 500 price index – November (Source: BCA Research as at 30th June 2023)

Average CIP performance over three months:

| Risk Profile | Q3 Average Performance | Highest performing | Lowest Performing |

| Adventurous | 0.77% | 2.86% | -1.17% |

| Mod. Adv. | 0.67% | 2.32% | -0.81% |

| Balanced | 0.33% | 2.07% | -0.67% |

| Cautious | -0.08% | 1.82% | -0.95% |

| Defensive | -0.37% | 1.70% | -1.52% |

| Benchmark Q3 Performance | |||

| S&P 500 | 0.63% | ||

| FTSE 100 | 2.19% | ||

Strategic Views

Despite only proceeding through three quarters of the year thus far, it is safe to say that 2023 has been a very unexpected year in terms of both the markets and geopolitical events. We have seen the technology sector, heavily influenced by the magnificent 7, lead the performance tables throughout Q1 and Q2, regardless of unfavourable market conditions with interest rates hikes, and still somewhat holding its own when the energy sector and US treasury yields outperform. As such, uncertainty looms larger than ever given global inflation is starting to fluctuate as borrowing costs and bond yields begin to rise, tapering the hope and anticipation of a ‘soft landing’. As you can see in the table on the whole the last quarter has produced positive returns within the different risk strategies which is positive news. If you have any immediate concerns or would like to further understand anything discussed in our investment reports, please contact your adviser and they should be able to give some further insight to your queries. Otherwise, we look forward to seeing you in our next meeting.

Past performance is not a reliable indicator of future returns. The value of investments and the income from them can go down as well as up, so your clients may not get back what they invest. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in small and emerging markets can also be more volatile than other more developed markets.